Welcome to our in-depth guide on bookkeeping mistakes. Whether you’re in the Common Small Business Mistakes industry or just starting, this article will break down what bookkeeping mistakes is, why it matters, and how to use it effectively.

What is bookkeeping mistakes?

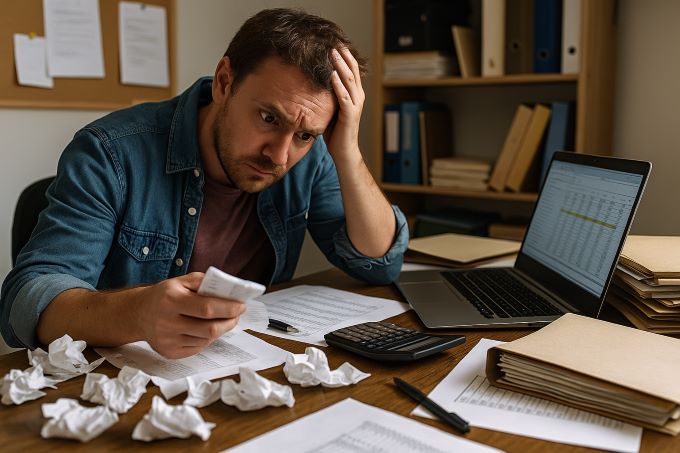

Accounting mistakes are described as errors happening while recording, arranging, and presenting the financial transactions of a business. These mistakes come from lesser entries mistakes to infarctions in compliance logs. For a small business bookkeeping context, these missteps may be quite damaging. They result in manifold financial and operational penalties-starting from the publication of a wrong tax result to that of incompetent financial forecasting.

Even the tech-savvy business owners using cloud-based accounting tools can make basic errors in bookkeeping. Quite many entrepreneurs underestimate the proper keeping of correct and accurate records; they will only come to realize their huge mistake when it’s expensive, maybe by lost revenue opportunities or, worse still, the penalties from relevant tax authorities. Learning what bookkeeping mistakes are makes the first step to ensuring sustainable financial health.

Why bookkeeping mistakes Matters for Common Small Business Mistakes

In today’s highly competitive business scenario, it is necessary for small-scale businessmen to become tight, clever, and very well endowed in knowledge. There isn’t any room for financial mismanagement any longer, especially if the source of mismanagement is often the most base mistakes in bookkeeping This is because bookkeeping is more than just maintaining records. It is the prime instrument to informed decision making, correct tax management, safe management of cash flows, and long-term growth of the business.

Bookkeeping mistakes yield an incorrect or incomplete financial picture about a company. For example, not reconciling accounts as regularly as it should be, or even if cash expenses are taken properly, these would seem like minor errors in the beginning. But the loss becomes very important if these mistakes cause one not to be able to know what profit margins are, prepare business growth, or accurately file taxes.

These problems crop up abundantly in the context of July 2025 as many small businesses upgrade or automate many aspects of their accounting processes without shaking up a very solid foundation there. Sustaining and managing the accounting software only can make reports erroneous and lead to considerable financial misunderstandings. Not only laws could be violated but potential erosion of trust from investors, partners, and even your very customers arises from such exclusions of financial integrity.

Real-World Examples of Bookkeeping Mistakes

This kind of example will show why details in authentic financial bookkeeping are important:

- Case 1: Misclassified Expense The wrong declaration of personal meal expenses in the corporate meals by a marketing agency repeatedly has resulted in $3500 penalty during post-audit due to inaccurate deductions that irreversibly damaged their reputation from the IRS. This is indeed a common form of error where entrepreneurs mix their personal expenses with their business expenses and do not follow rigorous documentation practices.

- Case 2: Disregarding Receipts A lawn-care service office often remembers purchases of small equipment below $100 without creating receipts. The result has been a disallowance of all those receipts for deduction at year’s end due to absence of documentation. The effect is an unexpected $2,000 rise in taxable income. It shows the importance of keeping all acceptable receipts, even if only for a petty acquisition.

- Case 3: Messed-Up Reconciliation A merchant reconciled its books every half-yearly towards reconciliation of their books thus resulting into an unnoticed fraudulent transaction with the business credit card, and unbeknownst to him, it led to a loss of $5,000 through identifiable fraud in the business credit card before, at length, it was later noted. An ordinary reconciliation would notice this within days.

Financial Clarity Leads to Strategic Growth

Above all, being able to correct small business bookkeeping serves as the entry point for growing smarter; because as transparent records would be, so would be timely reporting and up-to-date books, thus enabling you act faster, finance more easily, forecast with full confidence. Additionally, with changing regulation around digital and real-time transactions reporting by the time 2025, fewer and fewer chances will be left open for errors. While automatic tax enforcement and real-time monitoring payroll and AI-based audits could also catalyzing the transparency of business environmentally, it further did provide greater repercussions for any error.

Key Signs You Might Be Making Bookkeeping Mistakes

At some level, many of these bookkeeping systems may not know the extent to which they are put in dilemmas all over the project. Here are the signs to watch out for that could indicate you are making some common bookkeeping mistakes:

- Your financial statements don’t match your bank balances.

- Invoices are frequently paid late or missed entirely.

- Tax filings need frequent corrections or extensions.

- You or your team use personal credit cards for business purchases without logging the details correctly.

- You only check your books quarterly or annually, rather than monthly.

For those very early warning symptoms and awareness into proactive solutions, prepare to hire a part-time bookkeeper or go so far as integrating an automation accounting solution or even outsource accounting efforts. Further on in the second section, explore the top 7 grave bookkeeping mistakes small-scale business owners are committing and steer clear of them before these issues deal a deathblow to your company. Stay with us for the insights that could save your business time, money, and risk.

CTA: Avoid mistakes with our expert guide—explore the solutions to these common pitfalls in the rest of this article.

Common Challenges in Addressing Bookkeeping Mistakes

Widely known to avoid mistakes in bookkeeping, many businesses find it challenging to identify and rectify such problems at their budding stage, making them worsen problems. The main challenge is a lack of knowledge on bookkeeping. Small businesses typically have just one person, usually the owner, taking care of all the record-keeping duties in a business setting. Not having proper accounting training really affects it; you tend to mistake expenses for what they aren’t, or not record some income, or just put misinterpreted cash flow data.

A big part of it is inconsistency. Keeping proper records, all the time of everyday activities associated with small business bookkeeping—if too much time takes away from other business duties, they might not get performed. Not regularly scrutinizing a bank statement link with the accounting records, missing receipts, lack of journal entries, or even neglect of reconciliation can pile up their effects: financial reports that do not reflect reality make it challenging or even unmanageable to plan future budgets or make investment plans.

There is also a technology gap that undermines the effectiveness of bookkeeping. Even though modern accounting software like QuickBooks, Xero, and FreshBooks are available, not all business companies take full advantage of the software. Examples of such limiting factors may be limited automation, lack of integrations with payment systems, and underutilized reporting features.

Strategies to Correct Bookkeeping Mistakes

Correcting mistakes in financial records preparation for small business lies in regular systematic corrections. Put in simpler terms, the first thing to do is to scrutinize financial records-a task that a small business owner can usually do with proper advice of an experienced bookkeeper or CPA. Duplicated transactions, weird balances in the accounts that don’t match, or mismatched invoices and payments are possible things to look for. Further themes emerge as a pattern; a bunch of structural adjustments might be mandatory in the operation of the bookkeeping.

Reconciling as a habit, not just a single monthly job—this does not let down accounts at the bank or credit until far beyond error trapping. To avoid more manual work for yourself, automate the recurring entries and reminders in the accounting software. Additionally, the best practice in this case is a cloud-based system that operates in real time—cutting off manual entry issues since it can be reconciled with bank accounts.

Another important strategy is staff training. In case your employees have anything to do with financial data or documentation of expenses, they should understand what to do and why they have to be more accurate. Miscommunications of roles or lack of awareness from the employee regarding established compliance guidelines can lead to entry of mistakes.

How Bookkeeping Mistakes Impact Business Success

Failed efforts in addressing bookkeeping disasters tend to trickle down to other areas of the business as well. Financial reports are utilized in a score of important decisions-ranging from loans given and attracting investors to the design of pricing for a particular product. Faulty financial statements lead to bad decisions by owners, which could instead stop growth and even bring on the risk of insolvency in the company. Matters relating to taxation would also be very possible; wrong deductions and missing filings for taxes or underpaid taxes can lead to costly audits and fines.

However, the real paradox is such that recognizing and, therefore, rectifying the six most common bookkeeping errors may increase a businessperson’s confidence in decision-making. Timely data gives profitability visibility but on how to cut out unnecessary expenses and when to invest in expanding operations. Transparent records build stakeholder trust, be they banks, investors, or even suppliers, and may serve to boost one’s advantage in strategic negotiations.

Preventing Bookkeeping Mistakes Through Automation

Automation is changing the game for small business bookkeeping. Minimize human touch points in routine duties, reduce manual errors by almost up to 90 percent. All modern accounting software allows these things at the click of a button: an automatic invoice ing, of expense tracking, payment matching, and tax calculations. This not only prevents specific forms of mistakes in the accounting process but saves real time and resources for many others.

For instance, integrating your point-of-sale system or e-commerce platform with your bookkeeping software creates a synchronized environment where every transaction is automatically recorded. Real-time dashboards provide a better channel into understanding the health of your finances basis and opportunities for easy alert systems that ping you abnormalities like double entries or when cash flow dips suddenly.

However, there will always be the necessity of human oversight when it concerns automation. Full reliance on tech without regular audits can lead to unseen technical breakdowns or integrations that break. Thus, routine procedures by a human reviewer to verify whether the software still operates as intended ensure the integrity and accuracy of the system.

When to Hire a Professional Bookkeeper

Recognizing the right time you should employ a professional bookkeeper saves irrational and expensive errors to the business you have started. If your business is taking off quickly, has multiple streams of income, or is just running into tax complications, it is indeed worth the investment because a professional can offer you strategic insights, and align your financial records with the industry regulatory requirements—essential in “regulated” sectors like healthcare, law, or food services.

Another clear indication is the time you spend correcting errors than your actual business development. In this situation, then outsourcing or hiring an in-house bookkeeper can be really good solutions since herein you are really kept busy other things unless it’s some small considerations of yours..

Aligning Bookkeeping Practices with Business Goals

Bookkeeping should never be isolated from the general business strategy. All bookkeeping plans should be directed to either opening new markets, cutting overhead costs, or improving the workings of the cash flow forecast-thus very indicative that even a simple bookkeeping policy should support these outcomes. Key performance indicators linked with financial metrics-say, profits margins or accounts receivables days-must be put into place and effectively saw through via reports.

Through proper alignment of bookkeeping records with business intelligence, these smallest entities are able to figure out which portions of their actions yield the highest ROI. The said data-driven approach results in marketing budgets. Better aligned hiring decisions may flow from this realignment of resources, and finally, a really scalable growth model-all anchored in accurate and consistent financial tracking. When implemented properly, even the awareness of potential bookkeeping errors becomes more of a strength instead of a liability.

Preventing and Correcting Bookkeeping Mistakes

It is essential for every small business owner to understand how to avoid the common mistakes in bookkeeping. All of these range from very minor errors or faults in the records to larger lapses round compliance. However, a systemic approach should be adopted to basically spot and plug these issues long before their consequences snowball.

Best Practices to Avoid Bookkeeping Mistakes

The best way to avoid bookkeeping mistake is to put a control system in place. Here are prevention methods.

- Automate Task Processes Quantumly: Simplify the procedures, creating of accounting software data, such as QuickBooks and Xero, streamlines the invoicing tasks; yet it is difficult for anyone to commit an error.

- Conduct and Complete Reconciliation on a Regular Basis; the reconciliation should be completed monthly. It will help to show any error in the books between what appears in an account at the bank and what your books carry.

- Back-up records: Whether your accounting solutions are cloud and desktop based, backup of data would mean some form of protection against loss.

- Hire a Pro: Working with a bookkeeper specifically during busy seasonal times like tax season or in an extended growth phase, can save you from spending a lot on errors.

Red Flags That Signal Bookkeeping Issues

Estimates may sometimes declare that sometimes genuine firms also make certain red-flag errors. Early detection is crucial. Here are the telltale signs your bookkeeping may need an examination.

- There are regularly negative account balances in reports.

- Expenses are categorized far away from reality.

- It is difficult to get financial statements on time.

- Two bank or credit card statements have not been reconciled in four weeks.

If any of these signs sound familiar through your own books, then you might have to rethink your bookkeeping strategy in the business or meet with an accountant.

Why Consistency is Key

One of the most valued habits of bookkeeping is consistency. Regular recording, proper categorization, and appropriate review of those deals assist in minimizing surprise surprises and increase accuracy in projections. Inconsistent or sometimes reactive methods are likely to confuse your tax season or even for assessment of the performance of the business.

Leveraging Metrics to Guide Your Bookkeeping

Tracking changes in metrics – like cash flow, accounts receivable turnover, and profit margins – over time can thus reveal deficiencies in the art of bookkeeping. Most mistakes, such as low invoicing, late payment, or record-keeping lapses, are measurable through such seen benchmarks with numbers. Use accounting spreadsheets and reports automated through your bookkeeping software to keep abreast with your finance all year long.

Frequently Asked Questions

CTA: Master Your Finances Today

Don’t let bookkeeping errors hold your business back. Whether you’re just starting out or scaling your operation, following sound small business bookkeeping practices can ensure your financials stay in top shape.

Avoid mistakes with our expert guide — visit our detailed resources to get a step-by-step action plan tailored for small businesses.

- Explore our Small Business Bookkeeping Services

- Read 10 Essential Bookkeeping Tips

- IRS: Small Business Financial Resources

- Small Business Accounting Guide by NFIB